Learn the advantages of early planning and strategies if you’re starting late.

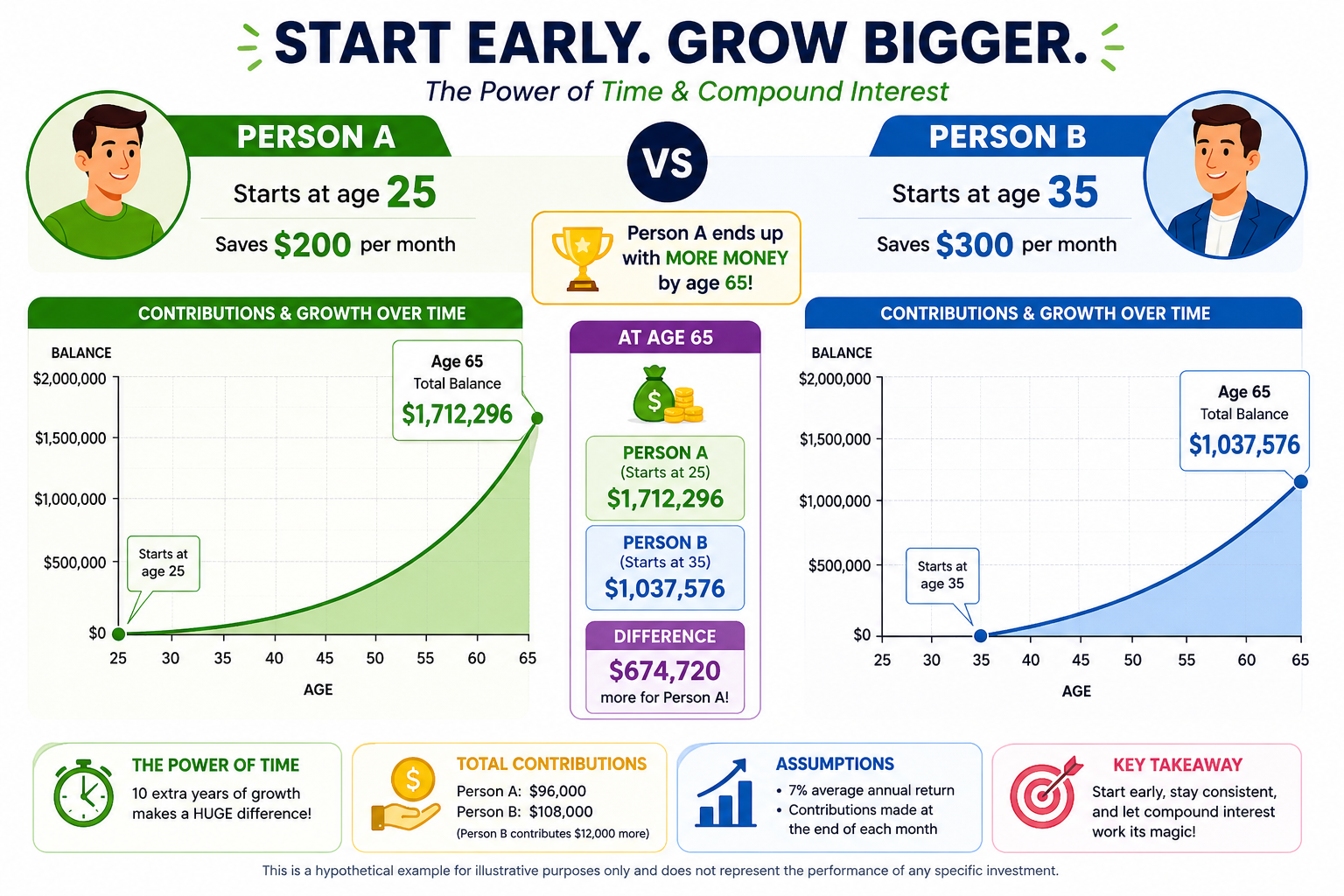

When it comes to building wealth for retirement, one factor matters more than anything else—time. Starting early gives your money the ability to grow through compound interest, where your earnings begin to generate their own earnings. This creates a powerful snowball effect that can turn small, consistent contributions into substantial wealth over time.

For example, imagine two individuals:

- Person A starts at age 25 and saves $200 per month

- Person B starts at age 35 and saves $300 per month

Even though Person B contributes more each month, Person A can still end up with more money by age 65—simply because their money had an extra 10 years to grow. That’s the power of starting early.

Starting young also reduces financial pressure. You don’t have to sacrifice as much from your monthly budget, and you gain flexibility to adjust your strategy over time. You can take calculated risks, recover from market downturns, and let time do most of the heavy lifting.

On the other hand, starting later—often in your 40s or 50s—means you’re playing catch-up. This requires a higher level of urgency and discipline. You may need to contribute significantly more each month, take advantage of catch-up contribution limits, and maximize employer-sponsored plans like a 401(k) to benefit from matching contributions.

Late starters may also need to rethink their timeline. Delaying retirement by a few years or waiting to claim full Social Security benefits can make a meaningful difference in long-term financial security.

The key difference isn’t just the amount saved—it’s the strategy. Early starters rely on time and compounding, while late starters must rely on higher contributions and efficiency. With less time to recover from market changes, risk becomes a bigger factor for those starting later.

Regardless of where you are today, the goal remains the same: build enough to sustain your lifestyle. A common guideline is the 70% rule, which suggests aiming to replace about 70% of your pre-retirement income.

Bottom line: Whether you’re ahead or behind, taking action now is what matters most. The earlier you start, the easier the journey—but even if you’re late, a focused plan can still get you there.